Alexandre Laumonier, Sniper in Mahwah

Addenda [12/7/13, 14:10:00:0001 EST]

Early October, more or less one week after Virtu published its own data about the Fed Robbery, a top representative of Virtu talked in front of exchanges top executives and said: “Nanex is peddling this nonsense about an early release. [Eric Hunsader] is just 100% wrong. … The problem is that the New York Post and CNBC and the Wall Street Journal and others pick this guy up as an authoritative source. And he really has and should have zero credibility. So what’s my upside? Do I go on CNBC, in one of these little boxes, and he’s going to attack me for this, that and the other thing? You know, I was probably responsible for the Kennedy assassination at the end of it, right? So we put our little thing out there and said our piece. He’s tweeting about it 24 hours a day, God bless him, but that’s the last you’ll hear about it from Virtu. But he’s wrong. Trust me, he’s wrong“.

God bless Nanex! I do not think Nanex was really involved in the Kennedy assassination (after all, we don’t know which was the speed – within a millisecond granularity – of the bullets); yes, Nanex may be a Twitter addict (what’s wrong with that?); yes, charts may lead to different interpretations (this is an epistemological problem); and yes, in this world no-one could be 100% right – but some could be 100% wrong. In the Great Fed Robbery case, hélas, it seems the McKay Brothers study proves without hesitation that Virtu is 100% wrong and Nanex is 100% right, period. Now, let’s move along.

[The post below was released from a secured lock-up room at 10:00:00:0000 am EST.]

Time & space

« To Milwaukee, Racine, Southport and Chicago. – We hail you by lightning as fair sisters of West. Time has been annihilated. Let no element of discord divide us. May your prosperity as heretofore be onward. What Morse has devised and Speed joined let no man put asunder ». This was the first telegraphic message received in Chicago, on January 15th, 1848 and it heralded 1848 as the “rise of the machine” in the Windy City. In February, the first steam-powered grain elevator replaced the old horse-powered elevators. In March, the Galena and Chicago Union Railroad started. In April, the Illinois and Michigan Canal finally opened for traffic. All these new technologies allowed Chicago to collect more and more grain from the prairie, culminating in opening of the first Chicago exchange to organize the trading of grains: the Chicago Board of Trade (CBOT).

Technology has always been crucial for exchanges as markets work with flows of information, and information needs to be transported. The first telegraphic message took eighteen hours to reach Chicago from Detroit, but soon speed was improved and information between the Windy City and New York could travel within a few seconds. Telegraph was seen as “the nervous system of the nation“, “a vast arterial system which carries the pulsation of the heart to the farthest extremity”, and played an important role in the development of the first “to arrive” products, as the product—let’s say, grains from the Midwest—could not reach New York as fast as the price of the product. Before the first official futures products were proposed by the CBOT in 1857, the “disentanglement” between the product and its price encouraged the traders in NY to think that the slip of paper with the price printed on it was the product itself.

« Time has been annihilated », said the first telegraphic tweet in 1848. A decade later, in his (then unpublished) Outlines of the Critique of Political Economy, Karl Marx wrote about capitalism as a machine which caused « the annihilation of space by time ». Perhaps Marx was right about space: in 2013, the Chicago Board Options Exchange (CBOE) is no longer in Illinois but in Secaucus, New Jersey. Geography has changed, but time has never been annihilated, and high frequency trading proves that: the space of the old pits became a matching engine, the old human traders became algorithms (in fact, a trader is a mix between human reason and non-human rationality), and an exchange is now a huge data center where algorithms are co-located close to the matching engine. If time were annihilated, we would live in the best of all possible worlds but there is an issue: an algorithm working from Manhattan will get information slower than an algorithm co-located in New Jersey data centers. So, the statement « let no man put asunder » is nothing but a dream. The algorithm located in Manhanttan is is rent asunder from the matching engine, and a milliseconds latency between them is now relevant. Time will never be annihilated… because of space.

If high frequency trading (HFT) is now a very discussed theme in financial markets, it is not really new. In an article published by the Chicago Democrat in September 1848, five months after the birth of the CBOT, there is a story about a Chicagoan who had raced down the docks after receiving word from the telegraph office that wheat prices were rising on the East Cost. He “immediately struck a bargain for a cargo at eighty cents per bushel… in less than fifteen minutes the market rose to eighty-five, and the fortunate possessor of the news by the last flash pocketed the cool five hundred“. The words “flash trading” were already in the mouths of Chicago speculators back in the 1850s! Telegraph allowed prices to equalize between Chicago and the rest of the US, but more informed agents (thanks to the telegraph provider Western Union, which was a fierce lobbyist when the CBOT made its new building in 1930) were able to do arbitrage at a faster speed. Nothing new with HFT–except that technical market microstructures became intricate and gave rise to new kind of information for “silicon traders“.

Microwaves & McKay Brothers

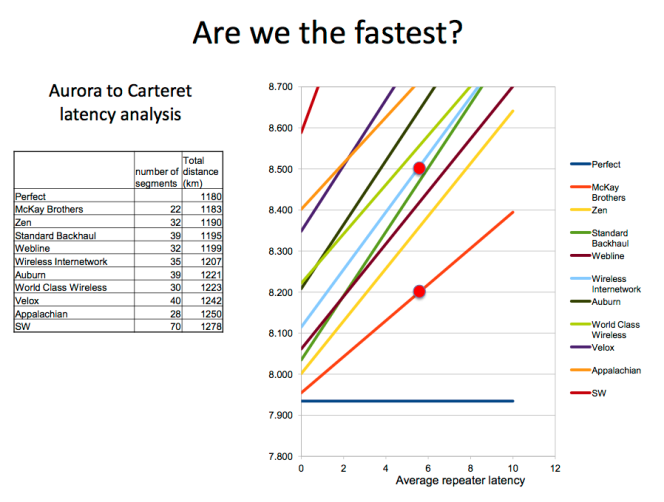

Albert Einstein showed us the scientific fact that a particule with information can’t not move faster than the speed of light, about 186 miles per millisecond in a vacuum. If stock exchanges want a level playing field, all exchanges should be located in one place on earth, but reality is different. Distance is a problem, and in the US the main challenge has always been the latency between Chicago exchanges (where futures are traded) and New York exchanges (where stocks are traded). Even if the CBOE is now in New Jersey, the CME and the CBOT (the two historical exchanges merged in 2007) still are in Chicago–in Aurora more precisely, where the CME Group has built its own data center. The Nasdaq exchange is located in Carteret, New Jersey.

« What built Chicago ? » asked a member of the CBOT in 1873. « Let us answer, a junction of Eastern means and Western opportunity ». The eastern opportunity was New York, and beyond New York, Europe–so grains could travel from Chicago to Paris. Chicago and New York exchanges have been tied up long before the telegraph was invented, but the latency has become crucial since algorithmic trading is now high frequency trading (see MacKenzie, Beunza, Millo & Pardo-Guerra 2012) . In the distant past, horses and pigeons were the fastest technologies to disseminate information. They were replaced by telegraph in the 19th century, and by optic fibers at the end of 20th century. Now, it is an old analog technology which seems to the fastest way to disseminate market datas/messages between Chicago and New York: microwaves.

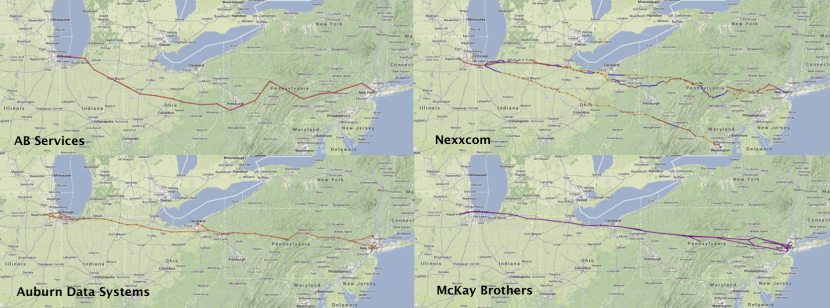

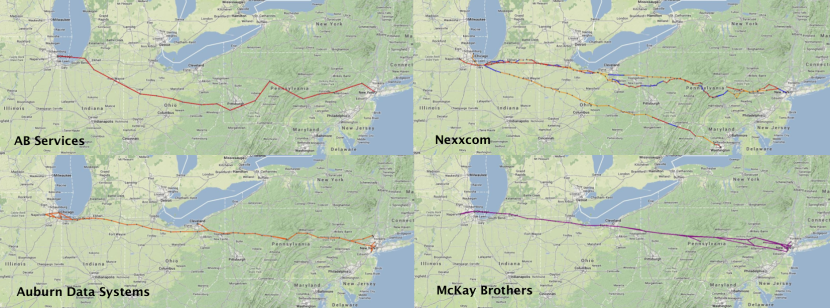

In a video presentation made last September at the Trading Show 2013 in New York, Stéphane Tyĉ, co-founder of microwaves network provider McKay Brothers, detailed the latest advances in the transmission of market data between Nasdaq’s home Cartaret and CME location Aurora. McKay Brothers claim their microwave path give them lower latency between the two places. Here are some maps from the presentation, with the paths of other microwave network providers based on the Federal Communications Commission datas, and the McKay Brothers path:

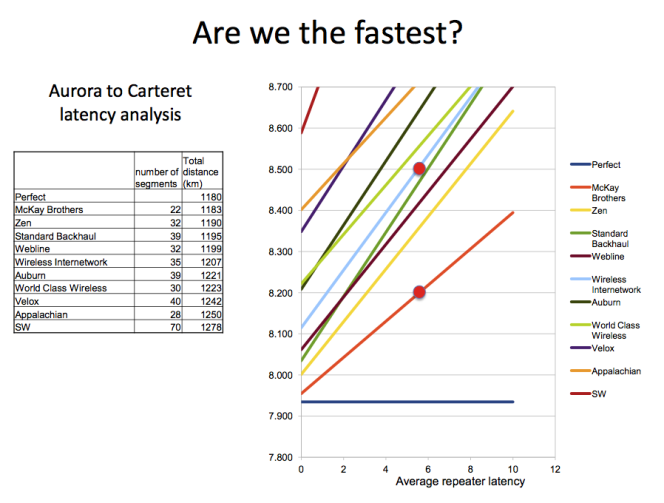

We can see that the McKay Brothers path is nearly a straight line. Here is another picture from the Trading Show 2013 presentation:

On November 25, 2013, McKay Brothers announced that in 2014 they will reduce their latency between Aurora and Cartaret to 8.147 ms. from 8.181 ms., thanks to the path “which has near zero deviation from the geodesic perfect arc” (here, latency is round trip time measured rack to rack). Quincy Data, market data service provider and parent company of McKay Brothers, proclaimed earlier in November 2013 that they could “deliver CME futures data directly into NASDAQ’s primary data center in Carteret, within 4.09 ms.“, that is 0.16 ms more than the estimated speed of light in vacuum between the two places, 3.93 ms. So, McKay Brothers seems to be the best microwaves transmitter for market data between the CME and Nasdaq, and if all algorithms were co-located in both the places, and if all those algorithms were clients of McKay, maybe we would have a level playing field. The long history of latency between Chicago and New York will probably end soon.

The Great Fed Robbery

However, information still has to travel in space. The Chicago-based market data feed provider and data analysis company Nanex known for its charts showing the “silicon traders” at work, recently discovered a discrepancy in the release of Fed/FOMC information on September 18th. As explained in July 2013 by CNBC journalist Eamon Javers here, the Fed has its own data center on 1275 K Street in Washington. On September 18th information should have been disclosed at 2:00 PM EST from K Street and then disseminated to the different US markets. Though the news was given to some reporters before 2:00 PM, the reporters were in a secured lock-up room presumably unable to leak information. But what Nanex data proves that Chicago and New York markets reacted to the Fed news so fast that is was physically impossible for the news to travel from Washington to both Chicago and New York. “When the information was officially released in Washington, New York should see it 2 milliseconds later, and Chicago should see it 7 milliseconds later. Which means we should see a reaction in stocks (which trade in New York) about 5 milliseconds before a reaction in financial futures (which trade in Chicago). And this is in fact what we normally see when news is released from Washington” wrote Nanex in its article “Einstein and the Great Fed Robbery”. Even with the fastest microwave network or supersonic carrier pigeons, Chicago and New York would not have been able to react so quickly.

The findings Nanex reported in “Einstein and the Great Fed Robbery” sparked a heated debate about what actually happened. HFT company Virtu responded September 25 by publishing their own study, which concludes that the “Nanex study is severely flawed.” Attacking the veracity of Nanex’s data, Virtu said, “it appears that the Nanex study relies entirely on the inaccurate SIP market data time stamps […] The Nanex data is clearly wrong because it is reflecting timestamps after the consolidation process has been completed by the SIP.” Though Nanex does use the publicly available consolidated feeds rather than raw feeds from exchanges, Virtu’s own data corroborates Nanex’s assertion that Chicago markets reacted in less than Virtu’s minimal time delay estimation of 2.1 ms. To obtain this 2.1 ms figure, Virtu too the straight line distance of 204 miles from Washington DC to New York City and the straight line distance of 595 miles from New York to Chicago to conclude that messages travelling from the Capitol to New York to Chicago should arrive with a nearly speed of light latency. The only network capable of transmitting data that fast is currently a microwave network. And, as Nanex notes, “reality is far from perfect”; microwave networks are not using perfectly straight lines, so “it’s a lot more complicated thatn simply using straight line distance and ignoring the realities of our world”.

McKay Brothers have revealed new realities about Nanex’s research into the “Great Fed Robbery”, and they don’t look good for Virtu – or the Fed. Minutes ago, at the Trading Show 2013 in New York, McKay Brothers co-founder Stéphane Tyc gave a talk entitled, “The Fed Robbery Revisited”. McKay revisited the debate with their own data sources–raw data feeds collected from Aurora and Carteret, the co-location centers for both CME and Nasdaq matching engines. While Tyc elaborated on the technical presets and results of their study, the details will be available tonight for further study. Following is an overview of information pertinent to this article.

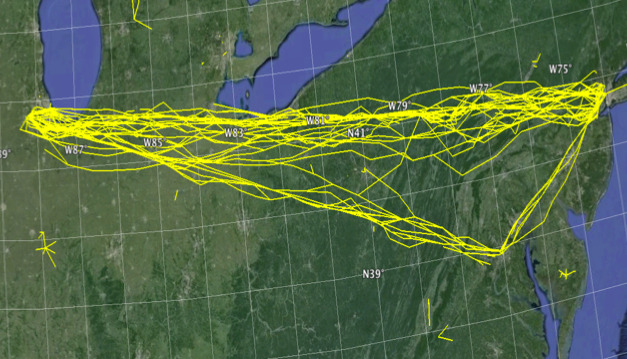

McKay assumes the news between K Street and Chicago/New York could travel through microwaves network, as shown below. For McKay’s own state of the art network, the distance between K Street and Aurora is 624 miles, and the distance between K Street and Nasdaq is 188 miles, so a message from DC should arrive in Chicago 2.34ms after arriving in New York rather than Virtu’s 2.1ms:

- A subset of FCC frequency applications identified by McKay Brothers as probable networks (© Stéphane Tyc/McKay Brothers)

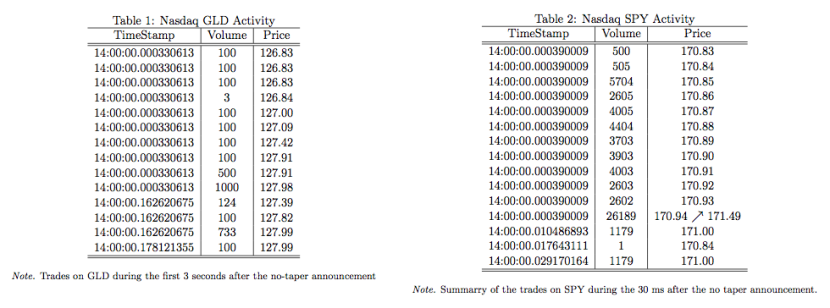

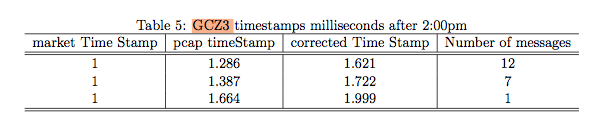

The first results of the McKay study show the trades on the gold ETF with most trading activity taking place on the same nanosecond timestamp, 14:00:00:00033613, and on SPY, which shows 155 trades time-stamped 14:00:00:000390009:

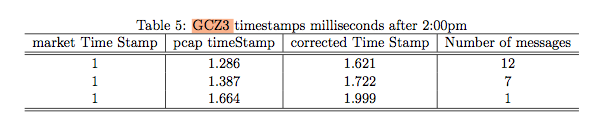

Nevertheless, due to technical reasons, those observations still could be consistent with a lockup release in Washington. McKay makes a distinction between a lockup news release, where information is locked-up in a room before 2 pm, and national embargo news release, where information is pre-loaded in various location and then released at 2PM at these locations. In order to have a more precise picture, McKay recovered microsecond timestamps in the markets’ clocks from their own inputs). They obtain the following results:

McKay concludes the Fed/FOMC announcement did not occur in DC; it was not a lockup release but an embargo release. Information was already in New York and Chicago before 2 pm. This confirms Nanex data with a more precise granularity, and is consistent with the statement made by the FIA PTG on October 2, 2013: “Starting in March, accredited media agencies have been given Federal Reserve policy statements in advance under embargo (as opposed to lock-up, as was the case prior to March). […] Since multiple media agencies have distribution points in Chicago and New York, the simultaneous release of the Fed announcement last week at 2:00 pm ET sharp in Chicago and New York (and simultaneous moves in those markets) should have been expected“.

Conclusion: the main issue is not raw data feeds versus SIP data, or microwave network versus optic fibers, etc., but the lack of clarity from the Fed about the news releases. Several reporters who disseminated Nanex’s findings were contacted by the Fed after Nanex uncovered the Great Fed Robbery, and we would be very interested to learn what the Fed told them. We would be happy if the Fed could explain publicly and precisely how the release of news works. Increased transparency would make the financial world a better place.